Find a Medicare Part D prescription drug plan

Medicare Part D

Prescription Drug Coverage 2026

Medicare Part D Premiums for 2026

As new legislation comes into play, Medicare Part D premiums

Understanding these possible changes could be crucial for making informed healthcare decisions.

Key Takeaways

- Medicare Part D premiums

in 2026 will likely be influenced by the Inflation Reduction Act, with potential changes in deductibles and costs varying by carrier.

- Income level will likely play a significant role in determining Medicare Part D costs, especially with the implementation of IRMAA, which may increase premiums for higher earners.

- Beneficiaries can utilize strategies such as switching plans, applying for financial assistance programs, and opting for generics to manage and potentially lower their Medicare Part D premiums.

Overview of 2026 Medicare Part D Premiums

As we look ahead to

While the act will likely aim to make medications more affordable, it might introduce a complex array of adjustments and policies that may affect Medicare beneficiaries.

Staying informed about these potential shifts could help beneficiaries make better choices for their healthcare needs with Medicare Part D plans and Medicare Medicaid services CMS.

Average Monthly Premiums by Carrier

Choosing the right Medicare Part D plan could significantly impact your healthcare expenses. The average monthly premiums by carrier may vary widely, likely reflecting differences in coverage and costs.

For Medicare beneficiaries, understanding these potential variations could be key to managing overall drug costs effectively.

Comparing premiums from different carriers may also help you find the most cost-effective plan. Keep in mind that lower premiums might come with higher out-of-pocket costs for certain medications.

Potential Factors Affecting Medicare Part D Premiums

Various factors will likely influence Medicare Part D premiums and understanding these could help beneficiaries make informed decisions. One factor might be the specific drug coverage plans and their formularies.

Plans covering a wider range of medications or more expensive drugs might have higher premiums.

Income level may also play a critical role. Higher earners will likely face increased costs due to the Income-Related Monthly Adjustment Amount (IRMAA). These brackets might be adjusted based on the Consumer Price Index for Urban Consumers (CPI-U), potentially leading to higher premiums for those with greater incomes.

Inflation rates may also play a significant role, possibly influence overall costs and potentially lead to premium adjustments. Additionally, shifts in drug prices and healthcare regulations could also impact Medicare Part D premiums.

Staying informed about these various factors and how they interplay could help beneficiaries make informed decisions about their healthcare coverage.

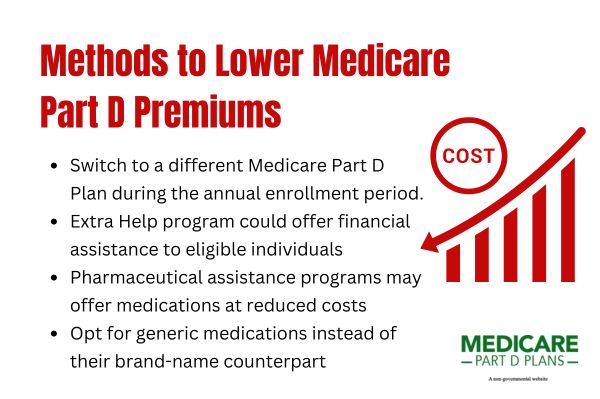

Methods to Lower Medicare Part D Premiums

Lowering Medicare Part D premiums may seem challenging, but several strategies could potentially help beneficiaries manage their costs effectively.

One approach may be to switch to a different Medicare Part D plan during the annual enrollment period. This period allows beneficiaries to compare plans and potentially find options with lower premiums.

For those eligible, the Extra Help program could offer financial assistance, possibly reducing premiums and out-of-pocket costs for certain medications.

Additional resources, such as pharmaceutical assistance programs provided by drug companies, may also offer medications at reduced costs for eligible individuals.

Another practical method might be opting for generic medications instead of their brand-name counterparts. Generics typically cost less while providing the same therapeutic benefits, likely making them a cost-effective choice for many beneficiaries.

Understanding Potential IRMAA and High-Income Surcharges in 2026

Income-Related Monthly Adjustment Amount (IRMAA) will likely impose surcharges on Medicare premiums for beneficiaries with higher incomes.

IRMAA calculations will likely be based on the modified adjusted gross income (MAGI) reported two years prior, meaning 2024 tax returns might be used

How to Calculate Your Modified Adjusted Gross Income (MAGI)

Calculating your Modified Adjusted Gross Income (MAGI) may be essential for understanding your potential IRMAA charges. MAGI consists of your total gross income. It may also include certain non-taxable Social Security benefits and other non-taxable income sources.

It will likely be derived from your Adjusted Gross Income (AGI) but might exclude tax-exempt interest and dividends from municipal bonds.

Calculating your MAGI for IRMAA purposes will likely involve considering all taxable distributions from traditional IRAs, 401(k)s, 403(b)s, and Social Security benefits. Careful calculation could help you anticipate additional surcharges and better manage your finances.

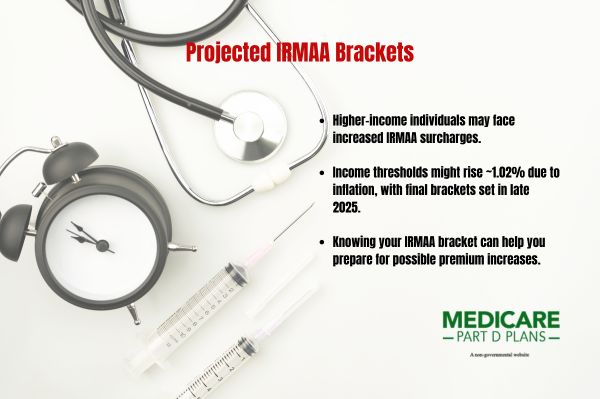

Projected IRMAA Brackets for 2026

The projected IRMAA brackets

These income thresholds might increase by about 1.02%, reflecting modest inflation annually impacts. The final brackets will likely be determined in the fourth quarter of 2025, based on the latest inflation data.

IRMAA brackets are structured into five income brackets, each with progressively higher surcharges. Understanding where your income falls within these brackets could help you plan for potential premium increases and manage your healthcare costs more effectively.

Strategies to Manage IRMAA Charges

Managing IRMAA charges will likely require strategic planning, particularly regarding your taxable income. Since IRMAA surcharges will likely be based on tax returns from two years prior, being mindful of your income and tax planning could potentially help mitigate these surcharges.

For instance, you might consider timing the realization of certain incomes to help avoid pushing yourself into a higher income bracket.

Another strategy might be to gradually increase your Medicare premiums based on your income, which could help incorporate IRMAA into your overall tax planning. Awareness of how your financial decisions impact your IRMAA charges could potentially provide savings in the long run.

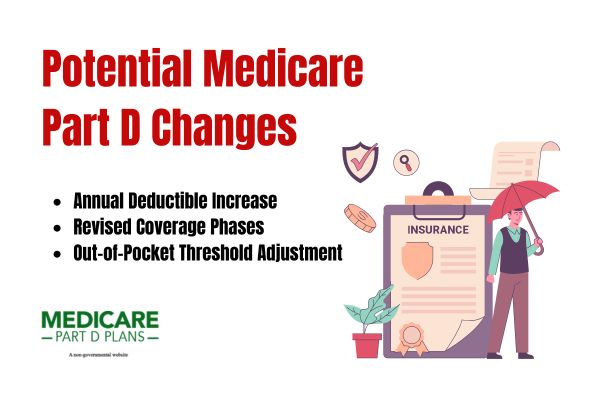

Possible Changes in Medicare Part D Program for 2026

The Medicare Part D program may undergo significant changes

These changes will likely be designed to make Part D prescription drug coverage more accessible and affordable for seniors.

Another possible change might be the cap on annual out-of-pocket costs for Medicare Part D enrollees, which may be set around $2,100.

This potential cap will likely be part of the broader effort to limit the financial burden on beneficiaries, possibly ensuring that medicare costs, drug costs, and cost sharing remain manageable.

Annual Deductibles

The standard deductible for Medicare Part D may increase to about $615. While any increase in deductibles may be challenging, this smaller rise will likely be part of a broader effort to balance costs and benefits for enrollees.

Understanding the potential implications of this increase could be crucial for beneficiaries. Higher deductibles might mean:

- Enrollees may need to pay more out-of-pocket before their coverage kicks in.

- Potentially higher coverage limits.

- Better access to medications once the deductible is met.

Out-of-Pocket Thresholds

Additionally, an out-of-pocket threshold for catastrophic coverage may be set around $2,100. Once beneficiaries reach this threshold, they will likely enter the catastrophic coverage phase, where they might not have to pay additional costs for their medications.

This potential threshold will likely provide financial relief to Medicare beneficiaries by capping the out-of-pocket expenses they must bear. Part D enrollees could potentially benefit from this cap, possibly making it easier to manage drug costs and avoid financial strain.

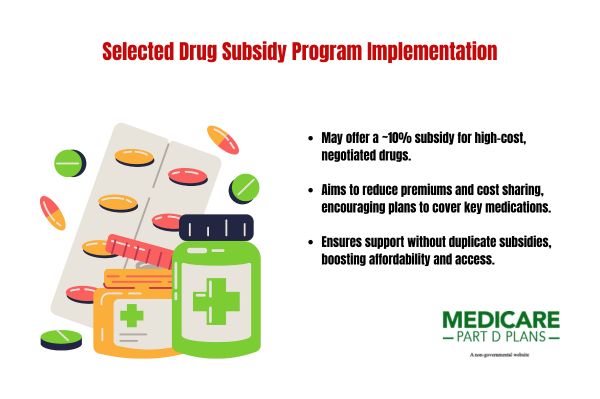

Selected Drug Subsidy Program

Starting January 1,

The subsidy might be applied to a percentage of the negotiated price for select drugs, which could help reduce overall costs for these medications. However, it’s important to note that a drug cannot qualify for both this subsidy program and the Manufacturer Discount Program.

See plans in your area instantly!

Advertisement

Comparing Medicare Advantage Plans with Original Medicare and PDP

Medicare beneficiaries will likely have several options for their health care coverage:

- Medicare Advantage Plans: Some plans may include additional benefits that could go beyond Original Medicare, such as vision and dental coverage. These plans may vary significantly in costs, with some offering lower premiums but higher out-of-pocket expenses for certain services.

- Original Medicare

- Standalone Prescription Drug Plans (PDPs)

Original Medicare, on the other hand, might not have an annual out-of-pocket spending limit, which could potentially lead to higher costs for beneficiaries with extensive medical needs.

Adding a standalone PDP to Original Medicare could help cover medications, but it may also involve higher premiums compared to Medicare Advantage plans that may include prescription drug coverage.

It’s also worth noting that certain Medicare Advantage plans may require referrals for specialist visits, whereas Original Medicare does not. Recognizing these differences could help beneficiaries select the most suitable plan for their healthcare needs and financial situation.

Potential Impact of the Inflation Reduction Act on Medicare Part D

The Inflation Reduction Act may bring significant changes to Medicare Part D, likely aimed at lowering prescription drug costs and enhancing benefits for beneficiaries.

One of the potential provisions of the act may be the ability for Medicare to negotiate prices for certain high-cost drugs, which could potentially reduce some out-of-pocket costs for medications.

Automatic Renewals for Medicare Prescription Payment Plan

This automatic renewal process will likely aim to simplify the management of prescription drug coverage for beneficiaries. However, those who wish to opt out of the automatic renewal process will have the option to do so.

If a beneficiary changes their Part D plan:

- They must opt-in again to the payment option with the new plan.

- Beneficiaries should opt into the plan at any time during the year.

- They must be aware that missing two consecutive payments could result in removal from the plan.

- After disenrollment, they can rejoin by contacting their plan.

Find a Plan and Enroll Online Yourself!

Advertisement

Summary

Understanding the evolving landscape of Medicare Part D premiums

By comparing different plans, calculating your MAGI, and utilizing strategies to help manage costs, you can make informed decisions that best suit your healthcare and financial needs.

As we move forward, understanding these potential changes is essential. Some of these developments may enhance affordability and access, possibly ensuring that Medicare beneficiaries receive the best possible care without undue financial strain.

Embrace these potential changes with knowledge and confidence, and you will likely be well-equipped to manage your Medicare Part D premiums

Frequently Asked Questions

How might the Inflation Reduction Act affect my Medicare Part D premiums?

The Inflation Reduction Act will likely be designed to lower prescription drug costs, which may lead to reduced Medicare Part D premiums for beneficiaries as it might include provisions for price negotiations and out-of-pocket caps.

Can I switch my Medicare Part D plan to lower my premiums?

You can switch your Medicare Part D plan to lower your premiums during the annual enrollment period. This allows you to select a plan that better fits your budget.

What is the out-of-pocket threshold for catastrophic coverage in 2026 ?

The out-of-pocket threshold for catastrophic coverage

How could the Selected Drug Subsidy Program help beneficiaries?

The Selected Drug Subsidy Program could potentially reduce certain medication costs for eligible beneficiaries by offering an approximate 10% subsidy on selected drug prices, starting January 1,

Begin Choosing your plan

Advertisement

ZRN Health & Financial Services, LLC, a Texas limited liability company.